The one question that has consumed my week

It has generated a lot of conversation but has a relatively simple answer

Hi there, my friend.

Last weekend, looking for a way to shake up the housing market, President Trump floated the idea of a 50-year mortgage.

I’ve talked and written about it a lot this week in my role of Chief Consumer Finance Analyst at LendingTree. It has basically consumed my week.

Here’s the question I’ve gotten more than any other:

“Is a 50-year mortgage a good idea?”

The answer, truthfully, is pretty simple.

While I can see the appeal and understand why it might be floated, the reality is that a 50-year mortgage isn’t a good idea in the vast majority of cases.

Here are two huge reasons why…

Reason No. 1: An astronomical amount of interest

To be clear, you generally pay a whole mountain of interest when you get a mortgage. Whether your mortgage is for 15 years, 30 years or possibly 50 years, it is typically the most expensive purchase you’ll ever make.

That said, the interest you’d pay on a 50-year mortgage could make those other mountains look like molehills.

This table from the report I wrote for LendingTree lays it out clearly.

Yes, you’re reading that right. If you take out a $500,000 50-year mortgage with a 6.1% interest rate — roughly the average for 30-year mortgages today — you’d end up paying $1.1 million in interest over the life of that loan.

$1.1 million!!

That’s nearly 2.5 times the original balance. It is also $420,000 more in interest than you’d pay for the same home with the same APR with a 30-year mortgage.

If that doesn’t make you think twice about the value of a 50-year mortgage, I’m not sure anything will.

Reason No. 2: Slow equity growth

Owning a home has traditionally been one of the most effective paths for people to build wealth. That’s because of something called equity. When you’re talking about a home, equity is the difference between how much you owe on a mortgage and what the home itself is worth.

For example, if you owe $400,000 on your mortgage but your home is worth $500,000, you have $100,000 in equity. You can then potentially borrow against that amount with a home equity loan or home equity line of credit (HELOC), both of which tend to have lower interest rates than credit cards and personal loans because they use your house as collateral. Those lower rates make them an appealing option for paying down credit card debt or financing big projects, though they’re not without risk. Putting your home up as collateral for a loan is never something that should be entered into lightly.

Equity grows when your home’s value grows, but it also grows when you pay down the balance on your mortgage. Put those two things together, and you’ve got rocket fuel for your equity.

With any mortgage, the process of paying down that original balance is slow. Most of your mortgage payment goes toward paying off interest rather than the original balance in those first few years. However, with a 50-year mortgage, the movement toward paying down the original balance is positively glacial.

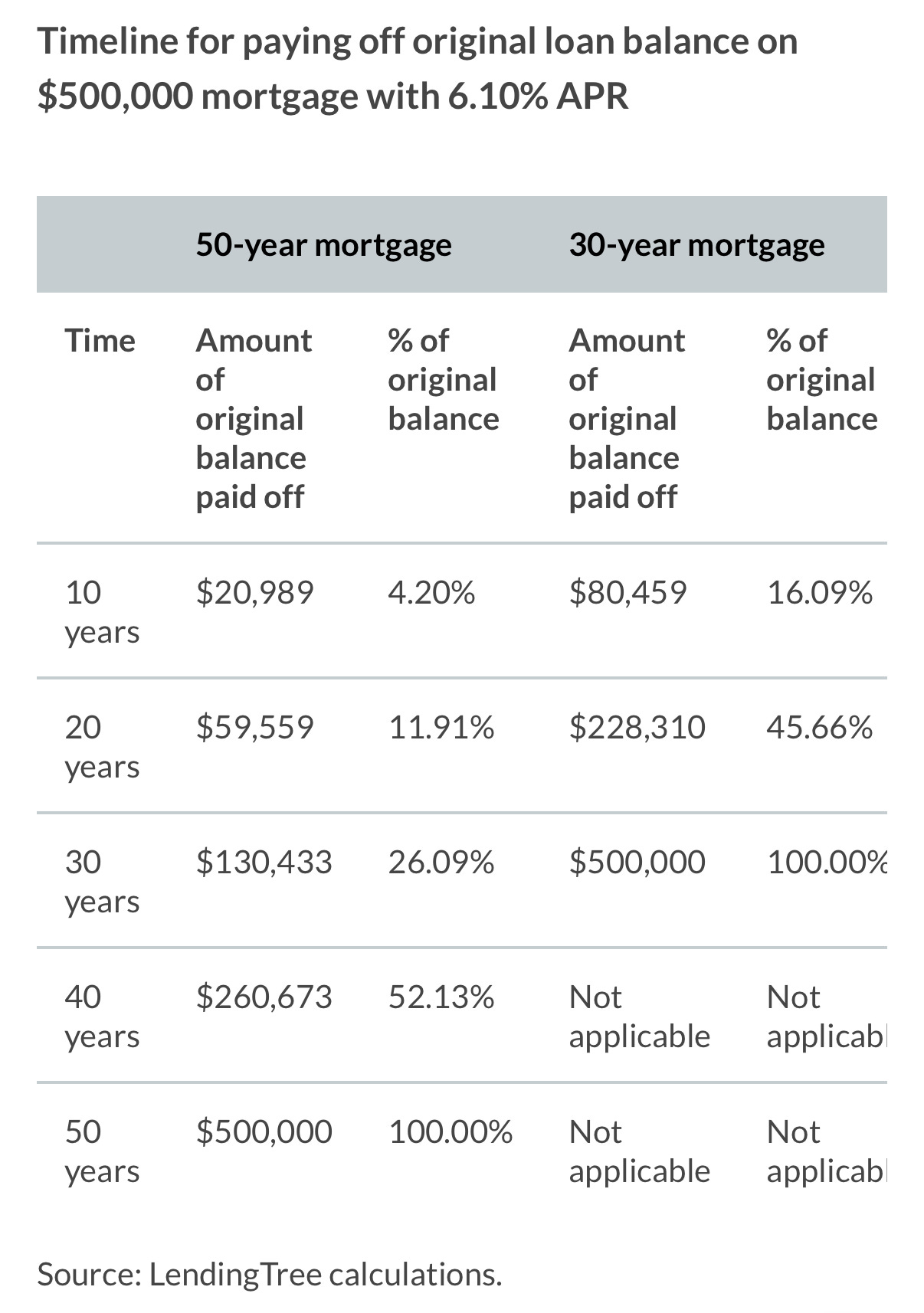

Here’s another table from my LendingTree report to illustrate…

After 10 years of paying on a $500,000 50-year mortgage with a 6.1% APR, you will have only paid down about $21,000 of the original balance. That’s about 4% of the total. Change that to a 30-year mortgage and you would’ve paid off more than $80,000 (or 16%) of the original balances.

That’s about a $60,000 difference in equity between the two!

Look out 20 years and the difference is even more stark. Almost $170,000!

Why would anyone ever do this?

After reading this, you’re probably wondering why I said earlier that I could see the appeal.

What exactly is that appeal then?

Lower monthly payments.

In today’s incredibly pricey housing market, that’s a big deal. Lowering a monthly payment by hundreds of dollars can be enough to turn the dream of owning a home into a reality.

The first table above shows a theoretical monthly payment on a 50-year mortgage. It is more than $250 lower than the payment on a 30-year mortgage with the same interest rate.

Still, in reality, it is unclear exactly how much lower the monthly payment would be. That’s because while the above example compares a 50-year mortgage with a 30-year mortgage with the same rate, that likely wouldn’t be case ultimately. A real 50-year mortgage would almost certainly have at least a slightly higher interest rate, meaning that the monthly payment and even the total interest paid would likely be at least a little higher than the tables show.

So, yes, payments would likely be lower. Low enough to make it worth paying hundreds of thousands more in interest? Most likely not.

The big takeaway

First of all, we don’t know if the 50-year mortgage will ever become reality. The idea hasn’t exactly been warmly received, even by the president’s supporters.

Still, no matter what ultimately comes of the 50-year mortgage, remember this…

If you’re good with paying more in the long run to pay less now, that’s your choice. However, it is essential that you understand exactly what those costs are before you sign on the line that is dotted. There’s simply too much at stake to do anything else.

That’s true with most any loan. It is certainly true about mortgages, but it applies to auto loans as well. We’re seeing people taking on longer and longer auto loans, for example. This CNBC report says that 22% of auto loans today are 84 months long.

As with mortgages, I understand the allure of lengthening the term to lower the monthly payment. However, with something that loses its value as quickly as a vehicle does, the math gets scary in a hurry, especially when you factor in all the extra interest you’ll pay. It is easy to see where someone could find themselves underwater on that car loan, owing more on it than it is worth. That’s a troubling proposition.

So what do you think? Would you ever consider one of these longer loans?

Until next time!

Matt

I think the 50 year mortgage is CRAZY for a multitude of reasons, but I can also recognize there are reasons why someone would choose it. It just feels so predatory!

A question about making mortgage payments has been on my mind and I wanted to put it out there for you. My mortgage is due on the 1st each month, but not "late" or any fees charged until the 17th. I should preface this by saying that I have never been late on a payment or charged a late fee for any property we've owned. Is there harm in paying after the first? I have occasionally floated the day my payment posts the first week of the month since I get paid every two weeks (more to help manage cash flow in my budget). It doesn't seem to impact my credit and my payments are all on time. If that's the case, wouldn't everyone just pay on the 16th?! I still consider the first to be the due date though and it would make me too nervous to wait until the last minute!